Raising Your Credit Score a Few Points Pays Off

Most lenders have strict standards when granting home loans to borrowers. Bankrate.com offers this example: If the best rates are available to borrowers with a 700 or higher credit score and your score is 698, the two-point difference will cost you thousands of dollars. On a $165,000 30-year fixed-rate mortgage, it is equivalent to more than $13,378 in interest charges, assuming a 4.5 percent interest rate with a 700 credit score and a 4.875 percent rate on a 698 score (Curry, 2015).So, what if your credit has some room for improvement? There are a few keys for preparing your credit so you are ready to buy a home at the best interest rate and terms.

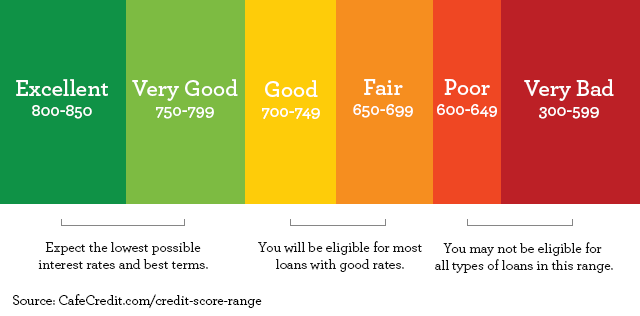

Get to Know Your Credit Score

As quoted on , Jeffrey Scott, spokesman for FICO, "The key to having the best FICO score possible is following three rules. Pay all your bills on time, every time, keep your credit card balances low and only open new credit when you need it (Curry, 2015)."

Knowing your FICO credit score is the first place to start. To get the complete picture of your credit, request your credit report from all three credit bureaus: Experian, Equifax and TransUnion. Your credit report is a comprehensive document showing your lines of credit, credit and loan balances, payment history and credit score. Many companies offer free credit reports. Examples include freecreditreport.com and Credit Karma.

What If Your Credit Report is Inaccurate?

Once you have all three credit reports in hand, thoroughly review them, first highlighting any errors. Reasons for credit report errors vary, but a few are credit abuse caused by fraud, an old collection account that should have been removed, or a mix up where someone with a similar name has filed bankruptcy or has delinquencies, but they are on your report. It happens.

Secondly, document omissions. For example, if a credit card has been paid in full but a balance is reported, follow up with the bureau(s) to get it corrected. If you notice a loan or credit card is not reported, notify the bureau(s) so your history is complete and accurate. Reporting missing data improves your credit score by providing a complete snapshot of your creditworthiness.

Build Your Credit Score with Good Habits

Several things can improve your score. If your credit score is low and your report is free of errors, understanding why is the next step. If you are a new borrower, it takes time to develop a payment history−six months is a good start but lenders may want more proof of your track record. If a credit card is your only credit-builder, diversify with an auto or personal loan. Lastly, avoid having multiple credit cards and using your entire credit limit. Overextending or using your maximum credit limit is viewed negatively by lenders. Pick one or two cards and manage them wisely.

More Helpful Credit-Building Hints

- Pay creditors according to their terms to build a positive credit rating. This includes monthly memberships, utility bills, and department store credit, as well as school loans.

- Pay rent on time and with a check or debit card so payments can be verified by your bank statements.

- Leave your oldest credit cards open to avoid looking like a newer borrower.

- Save, save, save. A typical cash down payment is between 5 to 20 percent. The higher your down payment, the lower your mortgage loan amount.

You Are Your Best Investment

You will never go wrong investing in yourself as a way to build credit to buy a home. It is in your best interest to know where you stand and work toward paying off creditors before trying to secure a mortgage to buy a home.

First, stop accumulating debt and prioritize what you owe. According to nerdwallet.com consumer debt (credit card debt, medical bills, payday loans and personal loans) should be your top priority to pay off (2016). Debts with lower fixed rates should follow.

Next, create a budget that includes saving and paying back your creditors. Ideally, you should be able to pay expenses, save for the future and pay down your debt. It may take longer to save your down payment, but you will be debt-free when you are ready to apply for a mortgage loan.

A smart-saving strategy is to have a set amount deducted automatically from your paycheck and deposited into your savings account.

Part of creating your budget is to assess what you can do without. Things like cable TV and gym memberships are not necessities while working a debt-reduction and savings plan. The money you save by cutting back on non-essentials is better invested when split between your debt and savings.

This brings us to the last step; working your plan. Once a debt is paid off direct your money to the next debt. Being consistent will produce your desired results and soon your consumer debts will all be gone, further establishing you as a creditworthy borrower.

Pursuing your dream of home ownership is incredibly difficult without an established credit history. The good news is you have a lot of control over your finances which determine your credit score. Using the credit-building strategies discussed in this article, you will prepare yourself to secure a mortgage loan and a new home.

Additional Resources:

How to Pay Off Debt: https://www.nerdwallet.com/blog/finance/pay-off-debt/

How to Get an 800 Credit Score: https://www.consumercredit.com/about-us/news-press-releases/2014/5-habits-to-get-800plus-credit-score/

How Much Home Can I Afford? Calculator: https://www.tdecu.org/resourcestools/calculators/mortgage/116-calculators/243-howmuchhomecalc.html

http://www.bankrate.com/finance/credit-debt/tips-for-boosting-your-credit-score-1.aspx